For years, I have been writing that healthcare spending would increase in the U.S. at an average annual rate of 6% through 2030, at which time it will total over $7 trillion (versus $3 trillion in July 2016) and represent 25% of GDP. Of note, the Centers for Medicare and Medicaid Services (CMS) has also forecast that healthcare spending should increase an average 5.8% through 2025 for reasons similar to those I citedemographics, medical advances, the Affordable Care Act and economic growth. The Congressional Budget Office forecasts that if present trends continue, healthcare spending will account for 37% of GDP by 2050.

During the ten-year time frame from 2015 to 2025, CMS predicts hospital care costs to increase by 80% to $1.8 trillion, and prescription drugs costs to increase by 91% to $615 billion. Total healthcare spending should approximate $5.6 trillion, suggesting that the pharmaceutical component will be 11%. I have maintained that focusing on drug costs will do little to contain aggregate spending growth due to its relatively minor contribution to the entirety.

The investment implications are significant. Healthcare spending is slated to grow much faster than the overall GDP. There will be increased demand for commodity medical products, pharmaceuticals (especially in oncology, hepatology, metabolic disease and neurology), less invasive surgical devices and healthcare personnel. From an investment perspective, attractive areas include hospitals, drug distributors, commodity medical product manufacturers, and hospital drug manufacturers, as well as pharmaceutical companies geared toward the specialty areas.

The Healthcare Spending Debate

As part of the presidential election cycle, there has been discussion about the expectation of substantial increases in health insurance premiums for 2017, especially as it relates to the Affordable Care Act plans. As I have previously written, a basic issue that needs to be addressed is the incentive structure of our system. In the private sector, those at risk (the insurers) can raise premiums to reflect greater payments. Other participants, including providers and manufacturers, typically benefit from increased utilization.

There are few options available to lower rising healthcare costs. The Sanders plan of "Medicare for all" is a potential solution, but I maintain that Americans are not willing to accept a government-run health plan at this time.

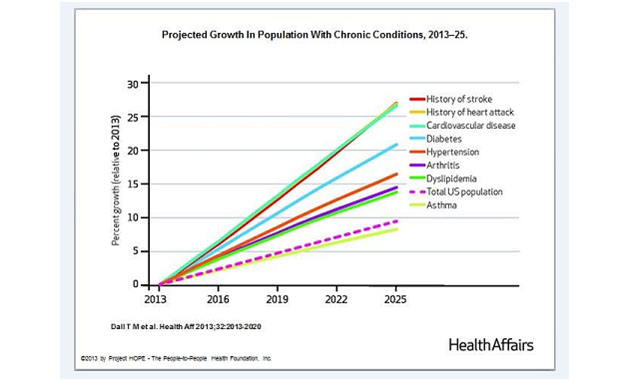

Another possibility is to "attack the problem at its source" by reducing the number of "disease units" per year, as opposed to the "cost per disease unit." This would necessitate focusing on preventable chronic conditions, including those that result from obesity and smoking, as well as end-of-life care. It is important to realize that 50% of healthcare dollars are spent on 5% of the population, so a targeted effort can result in dramatic savings. Furthermore, healthcare costs for those with a chronic disease are five times higher than for those without such a condition. As it relates to end-of-life care, it should be noted that 27% of all Medicare outlays occur in the final twelve months. We therefore need to form a task force of doctors, nurses, ethicists, clergy and caregivers to consider this very difficult issue.

With drugs only representing 11% of the U.S. healthcare spend, it would be shortsighted to focus solely on this sector and ignore the larger picture. While it is a populist notion not without validity, an effort to curb healthcare expenditures by imposing drug price controls would minimally impact the healthcare spending cost curve. Simply stated, prescription pharmaceutical spending, while readily experienced by most Americans, will not bankrupt Medicare, and controls in this regard will not prevent U.S. healthcare spending from representing 25% of GDP by 2030.

On Pharmaceuticals

With regard to pharmaceuticals, I view the problem as more widespread. Specialty pharmaceuticals, which represent 1% of prescriptions but 31% of the dollars, are a factor, as spending in this category is growing by 20% annually. This includes drugs for multiple sclerosis, arthritis and cancer, as well as for hepatitis C. These drugs often cost in excess of $100,000 annually, are complex to manufacture, and are frequently delivered intravenously or subcutaneously. Furthermore, it is estimated they represent 65% of spending on pharmaceuticals introduced between 2013 and 2015, and the pipeline of products suggests that this trend will remain. As an aside, in the 1990s, a drug was considered a blockbuster if its yearly sales exceeded $1 billion. I forecast that next decade, the new level of entry will be $20 billion, and it will be achieved.

The cost of pharmaceuticals is currently in focus due to political winds and absolutely inexcusable drug price increases. In my opinion, the latter issue relates solely to greed and avarice, and not in any way to advancing medical research. Importantly, these actions are not representative of the drug industry.

In focusing on the drug spend, much of the current problem with the high cost of pharmaceuticals relates to inaction in the last decade. Many orphan drugs have come to market since the 1983 passage of the Orphan Drug Act, which was designed to facilitate the development and commercialization of drugs used to treat rare diseases. It was believed that the small patient populations (less than 200,000) would preclude a reasonable expectation of profitability, and therefore incentives such as tax breaks, patent extension and enhanced marketing exclusivity were introduced.

In the past 30 years, over 2,000 compounds have received orphan drug designation, and involved companies have profited well due to the very high cost of therapy, which frequently exceeds $100,000 annually. I view the orphan drugs as most amenable to price reductions, as the considerable profitability of the companies appears to be in violation of the intent of the Orphan Drug Law.

Also, since 2000, many new drugs have been approved in oncology. Some, like Gleevec, extended life significantly and are recognized as breakthrough medications. Others only increased life expectancy by a few months, but were priced at $10,000 monthly.

During this decade, we have witnessed the introduction of several wonderful drugs, including some cancer immunotherapeutics that are more like Gleevec in efficacy. With a benchmark cost of $100,000 per year established by less therapeutic regimens, it seems disingenuous to expect these newer, superior drugs to be priced at a relative discount.

I argued similarly when Gilead Sciences Inc.'s (GILD:NASDAQ) Sovaldi was approved, as it was replacing a regimen that had lower efficacy, a greater side effect burden, a longer treatment duration and a cost of $75,000. There was strong objection when Sovaldi was priced at $84,000, but I maintained that precedent justified its cost. It seemed inappropriate to penalize Gilead for having a better drug.

Regarding specialty pharmaceuticals as a whole, I would mention that the first wave of biologics is slated to lose patent protection over the next five years. The FDA should be prepared to handle these applications in a timely fashion, and the companies with the branded drugs should think hard before filing patent extension lawsuits.

That being said, I believe that biologics will result in a second renaissance for the U.S. pharmaceutical industry, and that they will lead to meaningful advances in therapy in oncology, cardiovascular disease, inflammatory diseases and hematology. I would therefore not reduce market exclusivity, but would encourage more quality-adjusted life year (QALY) cost analysis to guide pricing decisions.

Solutions of the Healthcare Cost Crisis

In short, I believe that in the short term (next ten years), there is nothing we can do to contain the growth in healthcare spending. Over the intermediate term, there are three areas to focus on to restrain costs. Over the long term, we must reform the healthcare delivery system if we are to bend the cost curve sufficiently.

To impact healthcare spending in the intermediate term, we must either reduce the cost per "disease unit" or the number of such units. I believe there are three areas that can be examined for cost savings: obesity, cigarette smoking and end-of-life care.

Seven of the top fifteen medical conditions, including heart disease, hypertension, osteoarthritis and diabetes, are correlated with obesity, and it is estimated that an obese person spends almost $1,500 more each year on healthcare than an average weight person. The prevalence of obesity among adults aged 20-74 has increased from 15% in 1980 to 35% currently. Furthermore, it is estimated that 16% of those aged 2-19 are obese. We need to encourage healthier behavior (diet and exercise) from a young age, educate families on the benefits of reducing fats and "empty calories," urge restaurants to disclose caloric content and composition of meals, and support efforts focused on children exercising.

Tackling cigarette smoking will be more difficult, given political and personal sensitivities. It is estimated that the cost of smoking in the U.S. is $300 billion annually, of which $170 billion is direct medical costs. Analyzed differently, a pack of cigarettes costs $6.50, but the cost to society is $35. Cigarette smoking is the number one preventable cause of death in the U.S. I have long taken the controversial position that sales of cigarettes should be banned. However, by delaying a ban for at least a decade, the economic impact could be mitigated, workers could be retrained and land use could be reallocated. At the very least, I believe we should attempt to eliminate smoking in the presence of children, infants and pregnant women (while recognizing privacy rights).

Third, we as a society need to examine end-of-life care. Expenses associated with the last year of life (and even the last thirty days) are dramatic, and demographic trends are only going to exacerbate this issue. My recommendation would be to form a task force consisting of doctors, nurses, ethicists, clergy and caregivers, to consider this immensely difficult issue.

Ultimately, we shall have to modify the healthcare delivery model, especially given opposition to a national health plan. A basic issue that needs to be addressed is the incentive structure of our system. In the private sector, those at risk (the insurers) can raise premiums to reflect greater payments. Other participants, including providers and manufacturers, typically benefit from increased utilization. Implementation of best practice guidelines and greater use of preventative services should help, but the fragmentation of our healthcare delivery system limits their efficacy. Furthermore, advances in medical technology will continue to prolong life, creating even greater cost pressures. We as a society do not have the option of doing nothing, and the solution will only be more painful the longer we wait.

In Summary

Over the next 15 years, new drugs will greatly enhance the quality of life experienced by people with many diseases. My hope is that the companies that profit do so legitimately, investing in research and development and keeping drug price increases very reasonable, thereby rewarding both shareholders and patients. Unfortunately, independent of efforts to rein in the drug spend, our healthcare system needs to be reformed if we are to avoid serious consequences.

Dr. Len Yaffe has spent 30 years analyzing the healthcare sector, and he currently runs Stoc*Doc Partners, a healthcare hedge fund in San Francisco. He holds an MD from the Feinberg School of Medicine, Northwestern University.

Want to read more Life Sciences Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Statements and opinions expressed are the opinions of Leonard Yaffe and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

Chart provided by Len Yaffe